Homebuying tips FSBO

Condos Reward the Prepared Buyer

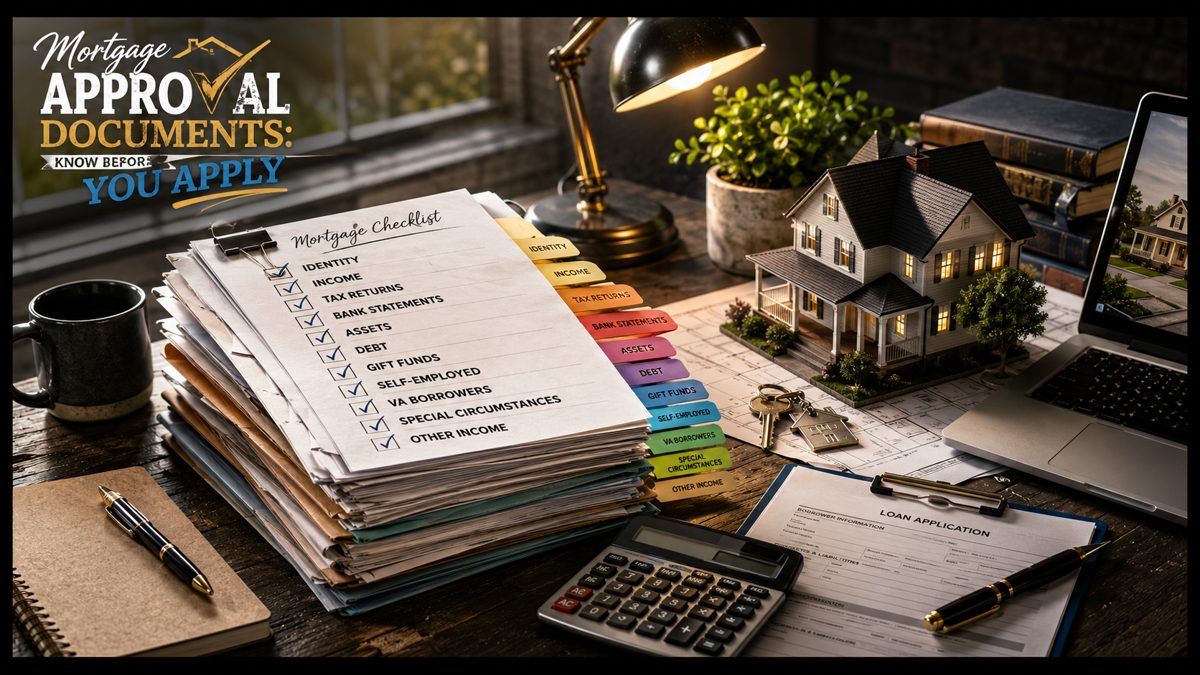

Mortgage Approval checklist

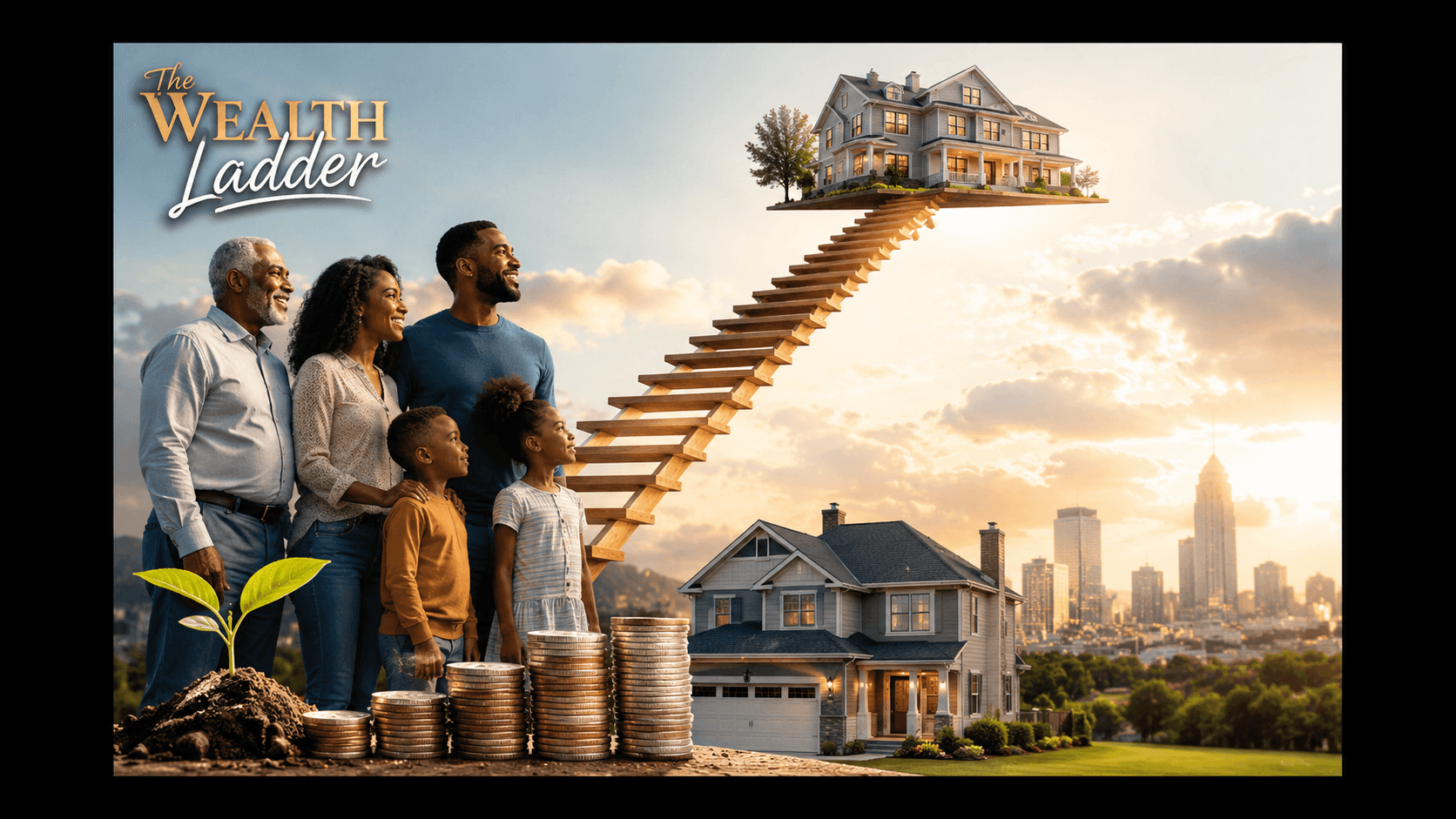

Homeownership builds wealth

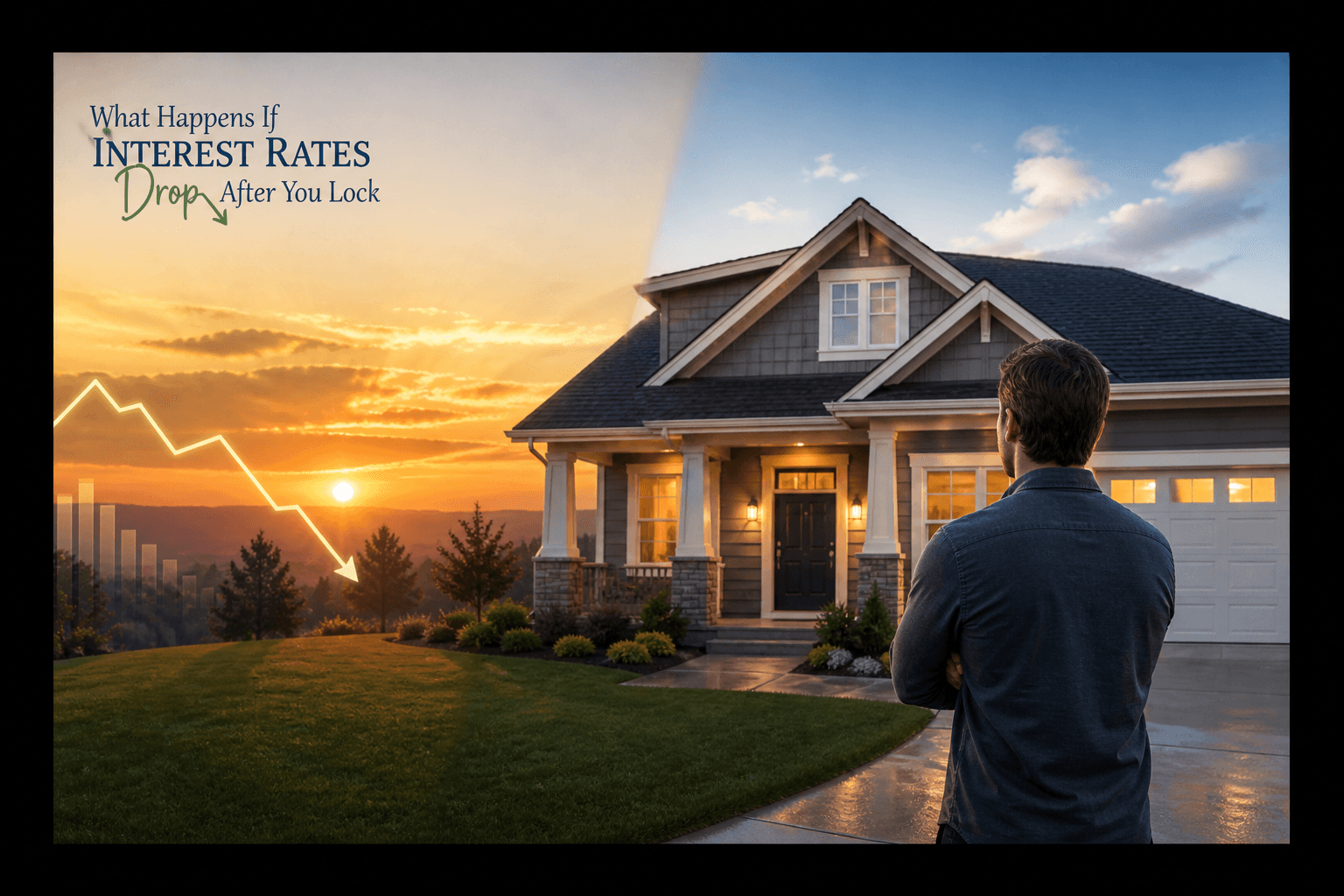

What to do if rates drop after you locked your rate?

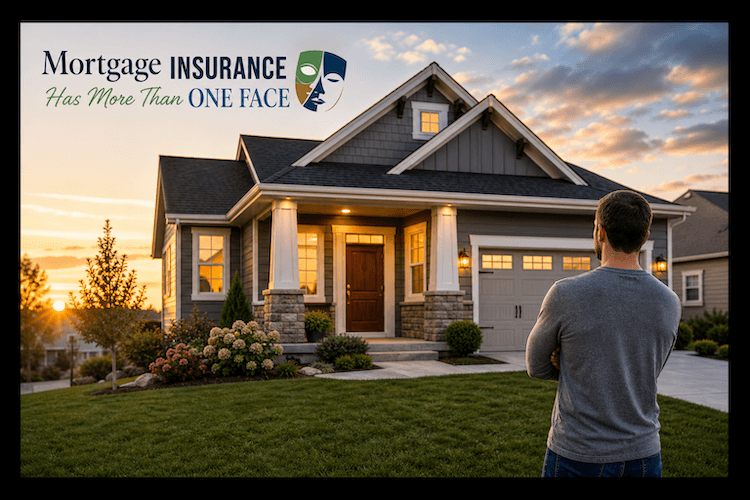

Mortgage Insurance Has varieties

Rate Shopping Mistakes

did you know your qualification does not depend on one score anymore?

Why Buying with higher rates is better than renting?